Introduction

Controlling food costs is essential if you are interested in restaurant profit margin. I'd like to discuss a few options for implementing controls over your food costs. In practice, there are many ways you can create a control. Let's start with a definition:

According to a website affiliated with the NRA, "The seven stages (of food cost control) are purchasing, receiving, storage, issuing, preparation, cooking, and service."

If you include retailing and selling under service, I agree. If your controls over food costs do not cover the activities of selling, or retailing, you are not seeing the entire picture.

Be careful when researching food cost controls. There are too many sites that think food cost control is simply the formula for calculating Actual Food Cost as a percentage of sales. While this formula is useful as part of a control, by itself it is simply a measurement.

Definition of Accounting Control

"Methods and procedures that are implemented by a firm to help ensure the validity and accuracy of its own financial statements." (Source: www.investopedia.com/terms/a/accounting-control.asp)

Controls are methods and procedures, and not simply calculations. Dividing responsibilities for a process between two or more people sets the stage for a control. For example, if the responsibility to order the food, is separated from the responsibility to pay for it, you have created a control. In this case, you have prevented one person from having the authority to commit fraud.

Measurements are what let us know if a process is working as planned, and whether the controls are working. For food costs, there are numerous measurements; beginning balances, purchases, transfers, recipes, prices of raw materials, and so forth. Three key measurements calculated by most back office systems are Actual (A) Food Cost, Theoretical (T) food cost, and the variance between these two.

Let's break down the seven stages of food cost mentioned at the top of this post across these. Purchasing, Receiving, Storage and Issuing are all parts of Actual Food Cost. Preparation, Cooking and a bit of Service are parts of Theoretical Food Cost. There is a piece of Service that is unaccounted for in calculating Theoretical food cost, and I will explain what that is a bit later.

Calculating Actual Food Cost

The Actual Food Cost measure of a raw material is typically calculated using this formula:

Beginning Balance + Purchases - Waste +/- Transfers - Ending Balance = Actual Food CostThere is a lot of work behind capturing all of these numbers. Inventory of all the raw materials needs to be counted at the start and end of the period. Transfers to and from other restaurants need to be recorded. And, of course, you have to record everything that is purchased and received at the back door.

But, there are other calculations used in the industry. The simplest, and perhaps least accurate, is using Food Purchases as the measure of Actual Food Cost. This is inaccurate principally because it measures how much material you bought, not how much material you used.

Accuracy is often the trade off when choosing your controls. Ideally, we want perfect accuracy with our numbers, but is perfection always affordable? I am not a fan of using Purchases as your Actual Food Cost, but it is a much easier calculation than counting inventories and recording waste and transfers. The question is whether the extra effort needed to be more accurate is worth it. The answer to that question is, it depends on your business. Is the average unit volume of your restaurant $3 million, or $300,000? The accuracy you can afford is probably different in those two situations.

Calculating Theoretical Food Cost

The Theoretical Food Cost measure is typically calculated using this formula:

Menu Item Recipe Cost (qty of the ingredients X cost of ingredients) X Quantity Sold of the Menu ItemMaintenance of the recipes is an never ending activity, not because the recipes change frequently, but because the costs and packaging of the raw materials may change on any day for any individual restaurant.

For example, imagine a recipe for a burger calls for 4 ounces of hamburger, and you buy the meat in 5 lb. containers and pay $15 for that container. Every time that menu item is sold, the food costing system reduces the theoretical inventory by 4 ounces of hamburger, and the system knows that cost you $1.00.

Now imagine that your supplier no longer carries your seasoning in 5 lb. containers, but 32 oz. bags. If you don't update your recipe to say that one purchased unit of seasoning just changed from 80 oz. to 32 oz., your Theoretical Food Cost will be inaccurate.

In most back office systems, every purchase made from every restaurant must be examined to identify any changes in package sizes, and the price for every ingredient. When a change is identified on an invoice, a corresponding change must be made to the back office system for that restaurant.

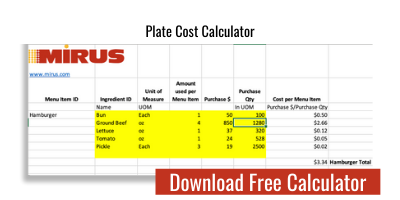

An alternative to this approach is the concept of Plate Cost. Plate Cost multiplied by the Quantity Sold of each Menu Item is summed to calculate the Theoretical Food Cost. The calculation of Plate Cost uses a recipe, but it is not calculated for every restaurant using the actual price paid for each ingredient at each restaurant. Instead, you use a spreadsheet to calculate Plate Cost using the average price paid during the period against a single copy of the recipes. The prices might be updated once per quarter or once a month, depending on the accuracy you determine is worthwhile. Less accuracy for significantly less cost and effort.

Calculating Food Cost Variance

Food Cost Variance is the difference between Actual and Theoretical Food Costs, and for many people the primary reason to use a back office system. So, what does it represent? Conceptually, Food Cost Variance is the food usage that is not explained by Recipes, Transfers, and Waste (if used in the Actual calculation). In other words,

Food Cost Variance = Missing Food.

Food Cost Variance = Breakage + Waste (if not in Actual) + Shrinkage + Portions = Missing Food

So, the question you might ask yourself is "Can I measure missing food directly"?

- Breakage and Waste can be tracked using log sheets

- Shrinkage comes in two forms, back door, and front door. Back Door shrinkage can be monitored using cameras. Front Door shrinkage can be measured by examining every check, every day for fraudulent behavior.

- Portions is the one piece that is not easily measured or monitored. Random sampling is one technique that will tell you, roughly, whether there too many or too few french fries in that basket.

So, the answer to the question is yes, you can measure missing food without maintaining recipes, pack sizes and ingredient costs by restaurant. And, in my next post on this topic I will explain the alternatives for measuring Missing Food with much less time, energy and cost of maintaining precise Theoretical Food Costs.

Summary

Controls are procedures that ensure the accuracy of your data. The effort put into a control step must be in proportion to the value of the item being controlled.

For many restaurant companies, the effort to maintain recipes, prices and pack sizes to calculate an accurate Theoretical Food Cost is too high. There are alternative controls that cost less and are more easily executed, albeit less accurate.

Looking for a better approach to controlling your food costs?

Thoughts?

Are you happy with the accuracy of your back office system?

About Mirus:

Mirus Restaurant Solutions is a multi-unit restaurant reporting software used by operations, finance, IT, and marketing.

For more information, please visit www.mirus.com

If you enjoyed this blog, please share this post by using the social buttons at the top of the page and make sure to leave your thoughts in the comment section below!

.png?width=50&height=50&name=Mirus%20Logo%20(1).png)