Keeping an eye on your Prime Costs is important to operating a successful restaurant company. Learn how to calculate and use restaurant prime cost and the targets you should aim for.

Keeping an eye on your Prime Costs is important to operating a successful restaurant company. Learn how to calculate and use restaurant prime cost and the targets you should aim for.

What is Restaurant Prime Cost

Simply put, prime costs are the combination of your restaurant’s products and people. These include the amount of money you pay for goods sold (COGS) which includes all beverages (alcohol and non-alcohol), and all payroll expenses for hourly staff, plus taxes and benefits.

Prime costs are important because they represent the expenses that are under your direct control and as such are also referred to as “controllable expenses.” While these are not the only controllable expenses you will incur, they do represent the largest percentage of costs that are under your direct control. Therefore, having accurate, timely insight into Prime Costs and understanding the factors that influence restaurant Prime Cost are critical.

Restaurant Prime Cost Formula

A restaurant's Prime Cost formula is computed as follows:

Cost of Goods Sold + Total Labor Cost = Prime Cost

$83,746.00 + $73,321.00 = $157,067

Restaurant Prime Cost Percentage

While the sum of COGS and labor costs is helpful it is best when viewed as a percentage of your sales. Why? Well, your prime cost calculation only tells you the money you are spending to operate. To better understand your Prime Cost’s impact on your business you’ll want to view it from a different perspective. To do that, you will also need know the Total Sales Revenue you generated.

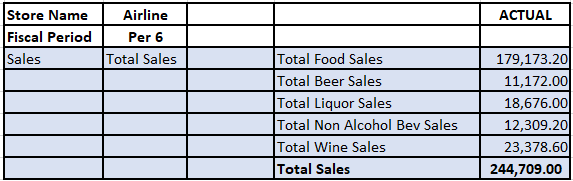

Total Sales Revenue Example

Once you know the Prime Costs for a specific time-period (day, week, etc.), and you know your Total Sales Revenue number for the same time-period, you can easily compute your Prime Cost Percentage.

Prime Cost Percentage Formula

To calculate Prime Cost Percentage, you must divide your prime costs (COGS + Total Labor) by your Total Sales Revenue. (Again, it is important that you use numbers from the same time periods before computing).

(Cost of Goods Sold + Total Labor Cost) / Total Sales Revenue = Prime Cost Percentage

$83,746.00 + $73,321.00 = $157,067 / $244,709 = 64%

When completed, your Prime Cost is now being shown as a percentage of your sales revenue. And while this is an important metric, it can be made even more powerful when added to your COGS, Labor and P&L reports. As you'll see in the example reports that follow, we've extended Prime Cost Percentages beyond the total by adding them to each category leading up to the Prime Cost total. Having this capability will further assist in understanding where costs are changing.

Cost of Goods Sold (COGS) Calculation

Cost of Goods Sold (COGS) – also known as Cost of Sales, is the amount of money your restaurant spends on supplies and ingredients for each of your menu items and it’s the first item subtracted from revenues.

To compute your COGS you’ll begin with your Beginning Inventory count which would be the amount of food and beverage in stock on the first date for the time period you’re looking to report on. You then add Beginning Inventory to the food and beverage items you Purchased during that same period and from that total you’ll subtract your Ending Inventory Count which, as you might suspect is the food and beverage items you have left at the end of the time period you’re reporting on. The calculation for COGS follows:

Cost of Goods Sold = Beginning Inventory + Purchased Inventory – Ending Inventory

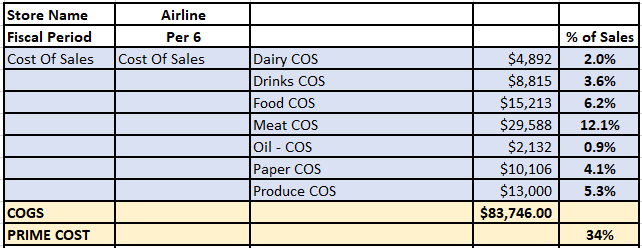

Following is an example of the COGS / Cost of Sales for one location (‘Airline’) for a specific fiscal period (‘6’). Please note, in this example the Food Cost Percentage has been added for each category to further help identify areas where opportunities exist to make improvements in Food Cost. It’s also helpful when looking back to see how COGS may be fluctuating or when a category is way over or under. Further, having the ability to produce and share similar styled reports with the Operations and Store Management teams on a weekly or intra-period basis will give them an opportunity to locate and correct issues, often before they can impact profitability.

COGS Example

NOTE: Food Cost Percentages must be determined accurately if they’re going to be useful. When done correctly, food cost percentages can be used to compare against both the industry and your prior performance, which can be used to help improve operations and your bottom line.

TIP: Here's an article talking about Restaurant Food Cost Controls.

Labor Expenses

While food cost is a major contributor, another major cost contributor are your labor expenses. Unlike COGS, some labor expenses are variable in nature, such as crew labor, and others are more fixed, such as manager salaries. Other labor expenses such as bonus payments are more discretionary, you pay them only when they are earned.

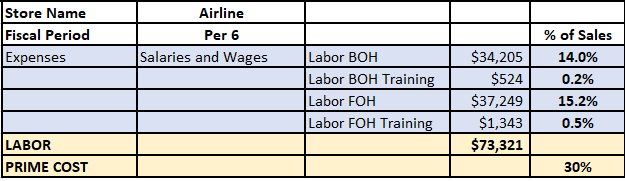

Labor Example

TIP: Here is a link to an article talking about ways to help control labor costs: Restaurant Labor as a Percentage of Sales is Foolish (Part 1 of 3).

What is a Good Restaurant Prime Cost?

In general, a profitable restaurant will generate a 25%-35% food cost and a 25%-35% labor cost. As you can see that's a pretty broad range so what does that mean? Well, it means all depends on the type of restaurant you are operating, the menu, staff, etc.

For example, fast-food restaurants often rely on foods that are expensive to purchase so, food costs can be slightly higher but, labor costs tend to be lower. On the other end of the spectrum, casual and fine dine restaurants generally have a higher cost of labor and, they purchase and offer higher quality food items on their menus which, in turn, allows them to charge higher prices. The net effect of this can be lower food cost percentages then some fast-food operators.

Prime Cost Percentage Examples

OK, let’s put that into perspective by looking at a fictional Quick Serve Restaurant (QSR). In this example, our fictional QSR restaurant generated $1,174,500 in Total Annual Revenue and its COGS were $357,000 and Total Labor $379,750. Using the formula for Prime Cost Percentage mentioned above this restaurant would have a Prime Cost Ratio of 63%.

($357,000 + $379,750) = $736,750 / $1,174,500 = 63%

Next, let's look at just the Prime Cost Percentage for their COGS:

($357,000 / $1,174,500) = 30%

Then, let’s look at a Fine Dine Restaurants (FDR) Prime Cost and see how it compares / contrasts to the QSR. Our fictional FDR generated an impressive $2,876,400 in Total Annual Revenue and had a COGS of $847,900 and Total Labor at $981,300. Again, using the formula for Prime Cost used above this restaurant would have a Prime Cost Ratio of 64%.

($847,900 + $981,300) = $1,769,200 / $2,876,400 = 64%

Now let's look again at just the Prime Cost Percentage for their COGS and see how it compares / contrasts with our fast-food example:

($847,900 / $2,876,400) = 29.5%%

As mentioned, FDR’s tend to use higher quality ingredients as well as a higher level of service. And while food costs may be higher than a QSR, often the food cost percentages can be lower due to higher menu prices.

So, back to Prime Cost Targets - as we saw earlier, restaurant Prime Cost Percentages can run as low as 50% and up to 70% with Fine Dine and Full Service restaurant running higher due to higher ingredient and labor costs. However, the generally accepted rule of thumb says that Prime Cost should run no more than 65% of total sales for full-service operators and 60% or lower is a good benchmark to keep in mind if you’re operating a limited-service restaurant.

Tip: Slightly lower in either case is better for achieving a healthier net income.

Caution!

When reviewing your Prime Cost Percentages, take note if your labor number is lower than expected as this could mean your table turns or throughput may be lower than necessary which will result in lower total sales, and worse, you may be underserving your guests, leading to dissatisfaction and possible loss of future visits.

Lower Food Cost Percentage may point to quality issues, another potential contributor to lost customers.

On the other end, profitability issues will begin to materialize as you begin to exceed 65% of sales and most certainly will for most as you approach 70%.

In the end, what might be a good Prime Cost Percentage for one restaurant operator may not be the same for another. As we mentioned earlier, it all depends on the concept, the operations, the level of service, menu, etc.

Other Controllable Expenses

Other controllable expenses is a category that includes items such as Marketing, Advertising, Admin, etc., and are the type of expenses that management can exert some control over. This could also include Consulting or Janitorial services provided they're not under some form of annual contract. Furthermore, grouping these expenses into categories like direct operating expenses, marketing expenses, supplies, etc., will make it much easier to identify where opportunities to cut costs might exist, should they be needed.

OK before we wrap up our discussion on Prime Costs, I think it's worthwhile to cover a few additional methods you can employ to expand on your Prime Cost calculations and yield other useful views of your restaurant's operations.

Before Tax Profit Percentage

Before Tax Profit Percentage is a percentage you can use to compare / contrast similar locations, determine if a location is worth continuing to operate, etc. This result is achieved by adding Overhead to your Prime Cost calculation.

Overhead costs are defined as the expenses that cannot be directly attributed to the production process but are necessary for day-to-day operations and unlike food and hourly labor these costs don't fluctuate based on changes in sales volume. So, overhead is any expense incurred to support the business while not being directly related to a specific product or service.

Overhead costs include:

- Rent

- Mortgage

- Salaries

- Loan payments

- Depreciation on building and equipment

- Equipment repairs and maintenance

- Utilities

- License fees

- Insurance premiums

- Etc.

Sales Revenue - (Cost of Goods Sold + Total Labor Cost + Overhead Cost) = Profit in Dollars

$244,709 - ($83,746.00 + $73,321.00 + $73,250) = $14,392

Profit in Dollars / Sales Revenue = Before Tax Profit Percentage

$14,392 / $244,409 = 5.8%

Prime Cost vs Conversion Cost – What’s the Difference?

OK, Conversion Costs are generally something associated with a manufacturing environment where the costs associated with producing components in one plant are computed and passed along to the next plant where that component will be used to produce a final product (sometimes referred to as Transfer Cost). So why discuss this in respect to the restaurant environment, well, I think most would agree that restaurants share a lot of similarities to manufacturing. In fact, when I think of restaurants in terms of manufacturing, I think of them as what's called Just In Time (JIT) manufacturing. JIT manufacturing is where you're using inventory to produce products in bulk and on demand - only in a restaurant it has to be hot, fresh, fast and accurate - take that manufacturing.

OK, enough of that, so where do I think Conversion Costs are applicable and useful, well, that would be in restaurant companies that operate a commissary. This is generally a separate facility where inventory is being prepped by its staff and the finished items are then transported to restaurants where they'll be assembled, packaged and delivered. Another possibility where Conversion Cost may come in handy is in restaurants that operate a buffet. So, what are Conversion costs and how do they differ from Prime Costs and why might I want to include this.

Well, let's first look at what Conversion Costs consist of - they include direct labor and overhead expenses incurred due to the transformation of raw materials into finished products that will then be transferred to individual restaurant locations where additional assembly will take place.

For example, your commissary is humming – produce is being chopped, dough is being prepared and rolled for pizza crusts or maybe bread is baking so it’s fresh and ready for those awesome sub-sandwiches your restaurant teams will be making at lunch. So, what makes up direct labor and overhead expenses?

- Direct labor costs are the same as those used in Prime Cost calculations.

- Overhead costs include: Rent, mortgage, salaries, loan payments, depreciation on building and equipment as well as equipment repairs and maintenance, utilities, license fees, insurance premiums, etc.

Whereas Prime Costs are expenditures directly related to the food cost and labor required to assemble, package and deliver the finished products – that finished pizza crust is topped with the freshly chopped produce, grated cheese and slid into the oven before it's boxed and delivered. Sandwiches are being stuffed with meats, freshly sliced cheese, and some of that same fresh produce….

Restaurant Conversion Cost Example

Summary

In the end, what might be a good Prime Cost percentage for one restaurant may not be the same for another. As we described earlier, it all depends on the concept, the operations, the level of service, the menu, etc. Regardless of the type of operation you run it's important to take time to become familiar with your Prime Cost numbers, so you'll be in a position to make adjustments as needed to improve / maximize your company’s profitability.

.png?width=50&height=50&name=Mirus%20Logo%20(1).png)